Identifying the Dimensions, Components, and Indicators of the Economic Justice Model in Iran's Budgeting System

Keywords:

Iran's budgeting system, economic justice, enemy-targeted economic justice, resistance economy, fiscal disciplineAbstract

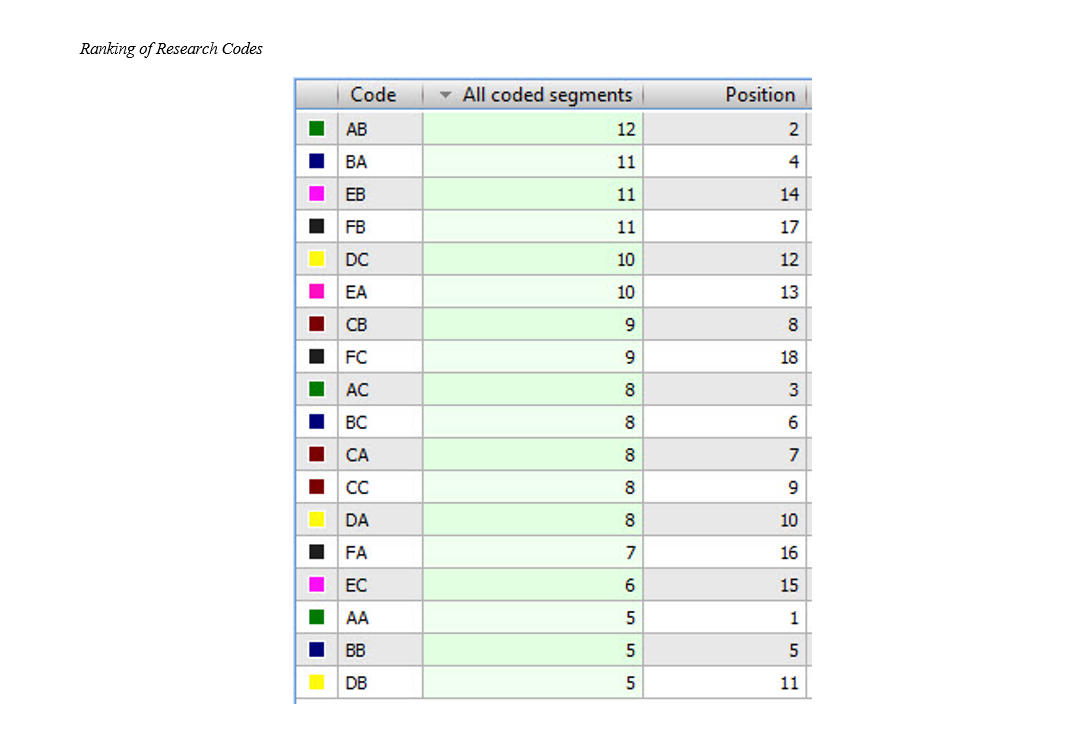

The objective of the present study is to identify the dimensions, components, and indicators of the economic justice model in Iran's budgeting system. From the perspective of its aim, this study is descriptive, and in terms of methodology, it is a qualitative descriptive research. Structured interviews were used for data collection. The statistical population included faculty members in the field of cultural management with over ten years of teaching and research experience, who also possessed executive expertise with at least five years of service or had conducted research on the culture of budgeting in the legislative and executive branches and economic justice in Iran’s budgeting system. Purposeful sampling was employed until theoretical saturation was reached, resulting in the selection of 15 participants from the target population. In the data analysis process, the content of interviews and textual data was coded using grounded theory methodology. The Maxqda software was utilized for qualitative data analysis and theorization. The findings revealed that the general structure of document analysis aligned with in-depth interviews, as displayed in the document browser section of the MAXQDA software, identified the following core variables of the study: enemy-targeted economic justice, resistance economy, fiscal discipline, corporate governance, commercial economy, and social economy. The concept of enemy-targeted economic justice includes indicators such as: fiscal unity, financial security, and elimination of political tendencies. The concept of resistance economy encompasses indicators such as: financial benefits, inequality index, and poverty index. The concept of fiscal discipline includes indicators such as: financial transparency index, development accounting index, and production accounting index. The concept of corporate governance comprises indicators such as: rentier state structure and financial and economic corruption index. The concept of commercial economy includes indicators such as: rent-seeking opportunity index and inefficiency index of private insurance systems. The concept of social economy incorporates indicators such as: inefficiency index of social support systems and unfavorable income status index.

References

Ahmadi, S., & Saidi, P. (2020). Identifying Future Drivers of Strategic Thinking for Managers in the Budgeting System of Iran with a Foresight Approach. Research in Planning and Development(5), 89-117ER -. https://www.journaldfrc.ir/article_129155.html

Al-Mahrouqi, A. D., & Mayada, M. (2024). The Robot Judge and the Development of Justice Systems Towards Algorithms. Journal of Legal and Economic Research (Mansoura), 14(0), 1185-1257. https://doi.org/10.21608/mjle.2024.386613

Ali, H., Imam Jom'e Zadeh, S. J., & Aghahosseini, A. (2018). Pathology of the Justice Model in the Governments of the Islamic Republic of Iran with Emphasis on Motahari's and Imam Khomeini's Thoughts. Scientific Quarterly of Islamic Revolution Research, 7(4), 67-95. https://www.roir.ir/article_85047.html

Ang, I., Isar, Y. R., & Mar, P. (2015). Cultural diplomacy: beyond the national interest ? International Journal of Cultural Policy, 21(4), 365-381. https://doi.org/10.1080/10286632.2015.1042474

Asghari, N., Es'haqi Gorji, M., & Abunoori, I. (2022). Modeling Budget Distribution in Iran Using Game Theory. Econometric Modeling(13), 133-153. https://www.sid.ir/paper/386710/fa

Bahrami, I. (2022). A Look at the Role of Accounting Information in Participatory Budgeting. Studies in Economics, Financial Management, and Accounting, 8(2), 80-97. https://civilica.com/doc/1728581/

Beyers, J. (2017). Religion and culture: Revisiting a close relativeJO - HTS Teologiese Studies / Theological Studies. 73(1). https://doi.org/10.4102/hts.v73i1.3864

De paula, T. M., & Mecca, M. S. (2018). Appreciation, preservation and promotion of local culture through the Creative Economy:the case of the production of gastronomic sourenir. Caderno Virtual de Turismo, 18(2), 116-128. https://doi.org/10.18472/cvt.18n2.2018.1321

Eker, M. (2012). The Impact of Budget Participation on Managerial Performance via Organizational Commitment: A Study on the Top 500 Firms in Turkey. Ankara Üniversitesi SBF Dergisi, 64(4), 117-136. https://doi.org/10.1501/SBFder_0000002139

Francis, H., Hasan, I., Song, L., & Waisman, M. (2013). Corporate governance and investment cash flow sensitivity: Evidence from emerging markets. Emerging Markets Review, 15(3), 57-71. https://doi.org/10.1016/j.ememar.2012.08.002

Kajouri Harj, J. (2019). Reforming and Reducing the Grounds for Rent Creation in the Budget Bill Approval Process in the Islamic Consultative Assembly of Iran. Research in Resistance Economy(7), 57-82. https://ensani.ir/fa/article/450115/

Kharkhan, M., Bahruloloom, H., Zaghiyan, H., & Andam, R. (2021). Identifying Factors Affecting the Implementation of Resistance Economy in the Sports of Public Universities in Iran. Journal of Research in Physical Education(33), 186-207. https://res.ssrc.ac.ir/article_2062.html

Larijani, S., & Kamali Rad, A. A. (2022). Examining the Military Budgeting Model of the United States and Proposing Solutions to Improve Military Budgeting in Iran. Defense Economics, 6(24SP - 1), 35. https://eghtesad.sndu.ac.ir/article_2246.html

Mahdavi, G. H., Hosseini, S. M., & Reisi, Z. (2013). The Impact of Corporate Governance Characteristics on the Quality of Earnings Forecasted by the Management of Companies Listed on the Tehran Stock Exchange. Management accounting, 16, 60-43. https://www.sid.ir/fileserver/sf/3971395h04236

Morteza Nia, H., & Sekhayi, A. A. (2020). Pathology of the Program-Based Budgeting Process: A Case Study of an Organizational University. Strategic Budget and Financial Research, 1(4), 45-67. https://ensani.ir/fa/article/461367/

Mousavi, S. F., Azar, A., Rajabzadeh, A., & Khadiour, A. (2018). Designing a Model for Performance-Based Budgeting Using a Combination of Soft Systems Methodology, Fuzzy Cognitive Mapping, and Fuzzy Hierarchical TOPSIS. Management Research in Iran, 22(1), 299-322. https://ensani.ir/fa/article/393743/

Namazi, M., & Rezaei, G. (2020). Presenting a Comprehensive Framework for Controlling Budget Surpluses in Government Agencies Using Strategic Management Accounting. Planning and Budgeting(150), 3-31. https://www.sid.ir/paper/414662/fa

Nikunhad, H., & Qarlagi, S. (2017). Institutions Violating the Principle of Non-Allocation in Laws and Regulations Governing the Budget. Public Law Studies(3), 44-70. https://www.noormags.ir/view/fa/articlepage/1325358/

Pourghafar, J., Zeynali, M., Mehrani, S., Mohammadzadeh Salteh, H., Pourghafar, J., Mohammadzadeh Salteh, H., Mehrani, S., & Zeynali, M. (2022). Presenting a Performance-Based Budgeting Model with an Up-to-Date Financial Reporting Approach in the Public Sector of Iran Investigating the Indicators Influencing the Establishment of Timely Performance-Based Budgeting in Iran. Public Accounting(16), 21-36. https://doi.org/10.52547/qjfep.9.35.169

Rahim, S. (2023). The Way Forward With Social Justice in Islamic Economics. International Journal of Islamic Economics and Finance Research, 6(2 December), 99-109. https://doi.org/10.53840/ijiefer129

Ramos, G., & Hynes, W. (2019). Beyond Growth: Towards A New Economic Approach. Economic, 55, 107-118. https://www.oecd.org/naec/averting-systemic-collapse/SG-NAEC(2019)3_Beyond%20Growth.pdf

Seyfollah, S., Sheikh, A., & Behdadfar, M. R. (2019). The Model of Economic Justice within the Framework of the Resistance Economy of the Islamic Republic of Iran. Journal: Strategic Defense Studies, 17(78). https://journals.sndu.ac.ir/article_717.html

Tabatabai Mirhosseini, R., Rouh Al-Amini Nejad, A., & Alavi, A. (2019). Budgeting Methods and Operational Budgeting in Government Organizations. Research and Islamic Studies, 1(5), 29-42. https://ensani.ir/fa/article/417378/

Taghvaee, V., Sharifpour, Y., Akbari, F., Arani, A. A., & Tatar, M. (2023). Integrated sustainability of social, environment and economy: Defining the hypotheses and theories interconnecting the pillars of sustainable development. In Reference Module in Social Sciences. Elsevier. https://doi.org/10.1016/B978-0-44-313776-1.00156-2

Takhtaei Shahi, M., Mohammadpour, R., & Hematfar, M. (2017). Strategic Financial Management by Identifying Necessary Factors for Establishing a Performance-Based Budgeting System in the Islamic Azad University of the Country. Strategic Management Research, 23(64), 134-151. https://www.noormags.ir/view/fa/articlepage/1236492/

Tohidi, A., & Alavi, H. (2017). Analyzing the Budgeting Method of the Country in Accordance with the General Policies of Resistance Economy. Strategic National Defense Management Studies(1), 204-239. https://issk.sndu.ac.ir/article_41.html

Zamani, R. (2017). The Budgeting System of Iran from the Constitutional Revolution to the Present: Based on a Personal Identity, Politically Balanced (but Ineffective) Along with Economic and Legal Imbalances. Economic StrategyVL - 6(22), 105-136. https://econrahbord.csr.ir/article_110138.html

Downloads

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2024 Manouchehr Mohammad Soleimani (Author); Mohsen Ameri Shahrabi; Ali Shojaei Fard, Serajeddin Mohebi (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.